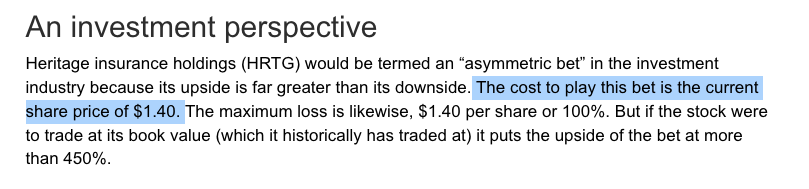

We released our first article on Heritage at $1.4 per share, currently, HRTG is at $3 per share.

What does the future look like for Heritage Insurance Holdings?

From FIU News “Florida’s insurance rates have almost doubled in the past five years, yet insurance companies are still losing money for three main reasons.

One is the rising hurricane risk. Hurricanes Matthew (2016), Irma (2017) and Michael (2018) were all destructive. But a lot of Florida’s hurricane damage is from water, which is covered by the National Flood Insurance Program, rather than by private property insurance.

Another reason is that reinsurance pricing is going up – that’s insurance for insurance companies to help when claims spike.

But the biggest single reason is the “assignment of benefits” problem, involving contractors after a storm. It’s partly fraud and partly taking advantage of loose regulation and court decisions that have affected insurance companies.

It generally looks like this: Contractors will knock on doors and say they can get the homeowner a new roof. The cost of a new roof is maybe $20,000-$30,000. So, the contractor inspects the roof. Often, there isn’t really that much damage. The contractor promises to take care of everything if the homeowner assigns over their insurance benefit. The contractors can then claim whatever they want from the insurance company without needing the homeowner’s consent.

If the insurance company determines the damage wasn’t actually covered, the contractor sues.

So insurance companies are stuck either fighting the lawsuit or settling. Either way, it’s costly.

Other lawsuits may involve homeowners who don’t have flood insurance. Only about 14% of Florida homeowners pay for flood insurance, which is mostly available through the federal National Flood Insurance Program. Some without flood insurance will file damage claims with their property insurance company, arguing that wind caused the problem. ”

Florida Insurance Risks

The first reason is just a risk shareholders must be comfortable accepting, because that is where the earnings come from. Premiums should naturally risk in tandem with risks.

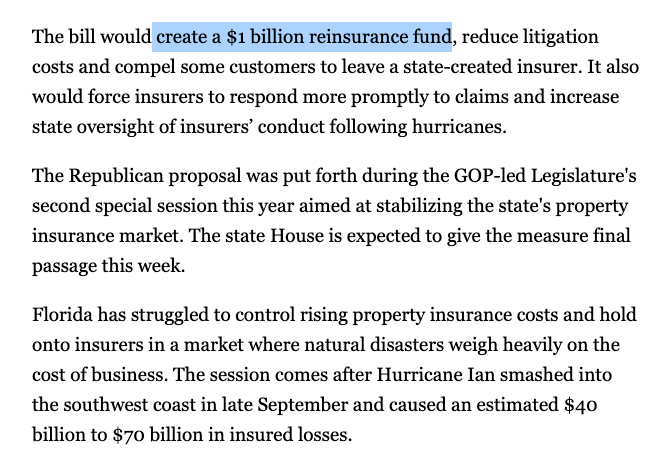

The Second reason is the private-reinsurance market. Increased prices making it more and more expensive for insurance companies to reinsure massive losses was eating into margins, and forcing insurance companies out of business. The new re-insurance fund will help Heritage, but not by much as reported in their latest quarterly earnings call transcript.

The third reason (abusive claims) is most favorable towards insurance companies in Florida. This has the potential to significantly reduce the number of claims paid to policyholders, thereby reducing loss ratios across the industry. The scope and magnitude of the abusive claims are uncertain, but it was enough to prompt HRTG’s management to completely disinvest from certain areas in Florida. We are quite excited to see the impact this has on future loss ratios.

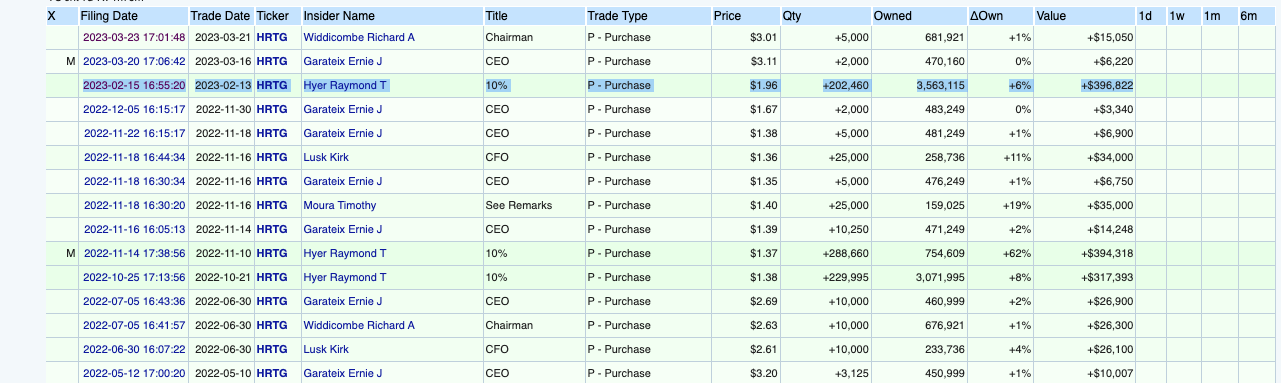

We are still seeing some *Token insider buying by management. Interestingly enough, Raymond T. Hyer increased his exposure when Heritage dipped from $3 to $1.96. It is currently back at $3, but he was also buying at $3+ earlier last year (2022). We are unsure of Raymond’s connection to Heritage, we only know that his company Futura Circuits Corp’s headquarters is located 12min (drive) away from HRTG corporate office. We believe he knows the management, but we have no evidence.

We remain bullish thanks to the reform we have seen and due to further insider buying from Hyer. It will be interesting to see what the next year brings for Heritage. If they do NOT have abnormally bad weather we may see income that approximates market cap.